When There Is A Change In Estimated Depreciation

As per the Accounting Standard 1- Disclosure of Accounting Policies the change in the method of depreciation is a change in the accounting estimate. New depreciation rate is.

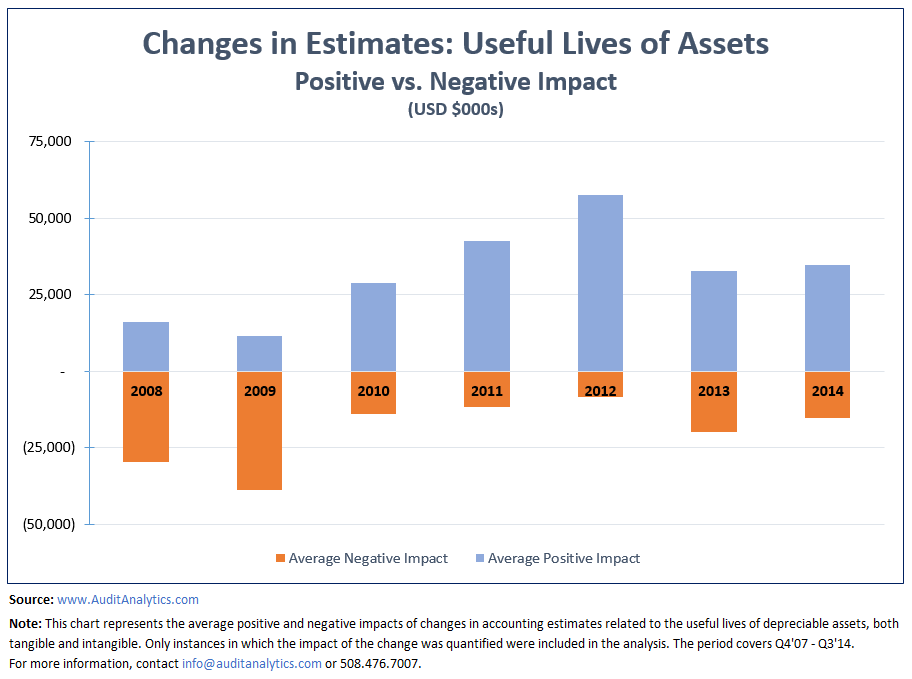

Changes In The Useful Lives Of Depreciable Assets Changes In The Useful Lives Of Depreciable Assets Audit Analyticsaudit Analytics

When there is a change in estimated depreciation the current and future years depreciation computation should reflect the new estimates.

When there is a change in estimated depreciation. When there is a change in estimated depreciation. A previous depreciation should be corrected. Changes in the amount of expected warranty obligations.

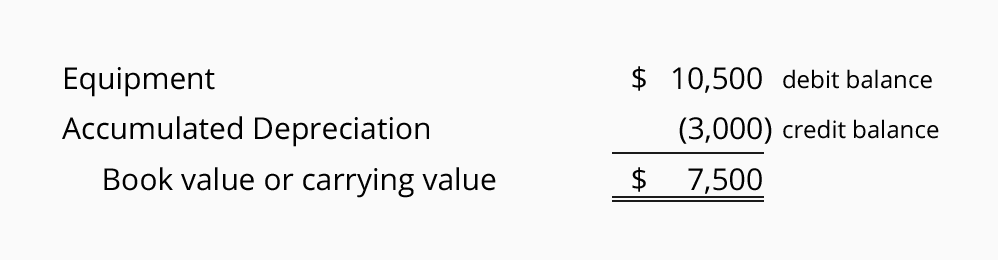

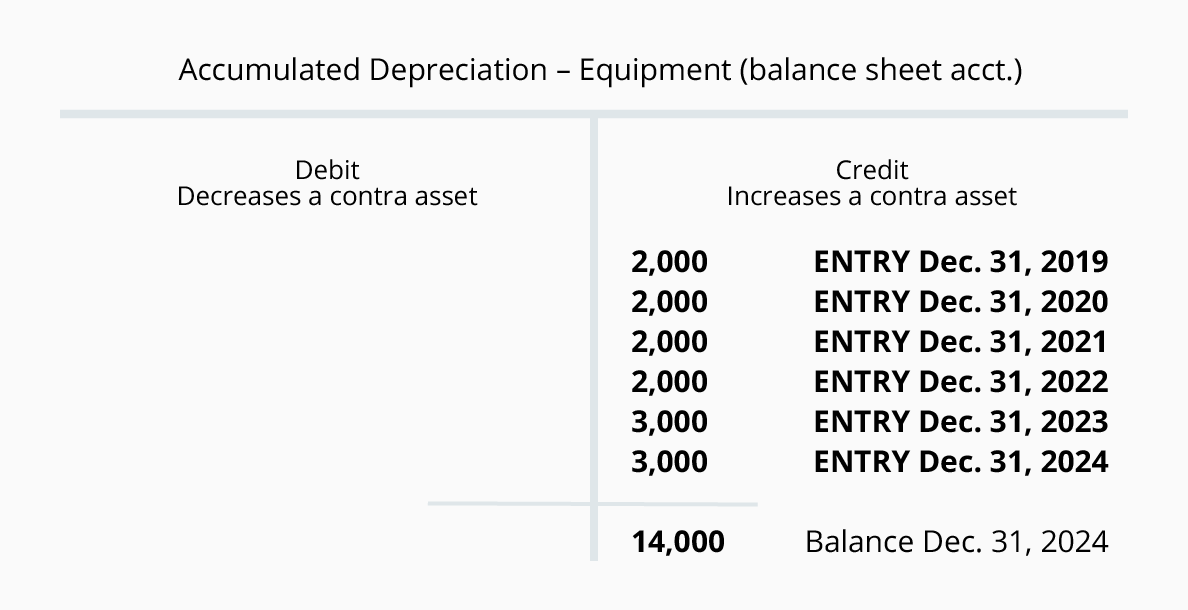

A previous depreciation should be corrected. On december 312014 before adjusting entries had been made the company decided to change the remaining estimated life to 4 years including 2014 and the salvage value to 2000. Is depreciation an accounting estimate or policy.

D None of the above. Previous depreciation should be corrected. When there is a significant change in the pattern of the future economic benefits from the asset then the method of depreciation should also be changed.

As per the Accounting Standard 1- Disclosure of Accounting Policies the change in the method of depreciation is a change in the accounting estimate. When there is a change in estimated depreciation. On the same footings change in depreciation method is not a change in accounting policy rather it is a change in accounting estimate.

Allowance for doubtful accounts. B current and future years depreciation should be revised. Reserve for obsolete inventory.

Change will be implemented from the date of revision and onward. However revenues may be impacted by higher costs related to asset maintenance and repairs. When there is a change in estimated depreciation.

What happens when there is a change in estimated depreciation. Answer of When there is a change in estimated depreciation. When there is a significant change in the pattern of the future economic benefits from the asset then the method of depreciation should also be changed.

Whilst commonly referred to as a depreciation policy the depreciation method used is actually an accounting estimate as detailed in FRS 102 paragraph 1723. Changes in accounting estimates result from new information or new developments and accordingly are not. A change in estimate should not be accounted for by restating amounts reported in prior period financial statements.

New plant assets should be acquired to replace the old. It was originally depreciated on a straight-line basis over 10 years with an assumed salvage value of 12000. A previous depreciation should be corrected.

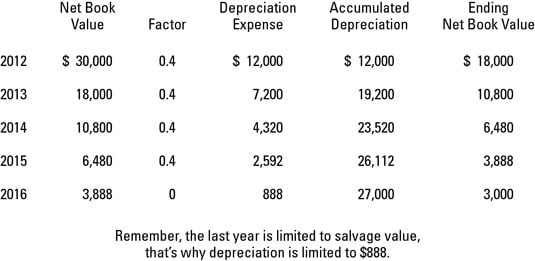

A change in accounting estimate is an adjustment of the carrying amount of an asset or a liability or the amount of the periodic consumption of an asset that results from the assessment of the present status of and expected future benefits and obligations associated with assets and liabilities. The high salvage value limits the cost to be allocated. A previous depreciation should be corrected.

Although the total depreciation expense over the course of the assets life is the same 500K the impact to the period in which the change was made was a relative decrease in depreciation expense of 32K. If the change affects the period in which the change is being made and any future periods then the effect should be accounted for in the period of change and in the future periods being affected. Changes in the salvage values of depreciable assets.

This is known as depreciation and there are several different depreciation methods which allow businesses to determine the projected loss of value of certain assets over time or based on actual physical usage. Bcurrent and future years depreciation should be revised. B current and future years depreciation should be revised.

What was the depreciation expense for 2014. The effect upon the income statement for a change in estimate that affects several future periods. Changes in the useful life of depreciable assets.

When there is a change in estimated depreciation current and future years depreciation should be revised only future years depreciation should be revised new plant assets should be acquired to replace the old. When there is a change in estimated depreciation the current and future years depreciation computation should reflect the new estimates. What should be done when there is a change in estimated depreciation.

A high estimated life spreads the cost over a longer period of time resulting in a smaller expense each year. Thus it requires quantification and full disclosure in the footnotes. Asked by Djjensen Last updated.

Calculation of depreciation expense involves estimation of several elements that may change or require revision during the life of asset due to internal or external factors. C only future years depreciation should be revised. When a change in the useful life estimate occurs there is no need to make a journal entry.

Change in the useful life estimate does not represent an accounting error. Estimate changes are an inherent and continual part of the estimation process. All of the following are situations where there is likely to be a change in accounting estimate.

Changes in Accounting Estimates must be accounted for prospectively in the financial statements ie. Become a member and unlock all Study Answers Try it risk-free. The answer however depends on whether the change is a change in estimate or a change in accounting policy.

Only future years depreciation should be revised. Change in accounting estimate. When there is a change in estimated depreciation.

Current and future years depreciation should be revised Current and future years depreciation should be revised - ProProfs Discuss. With that change in the assets estimated useful life the company would now recognize 18K in depreciation expense on this asset each year for the next 25 years. B current and future years.

Therefore carrying amounts of assets and liabilities and any associated expense and gains are adjusted in the period of change in estimate. B current and future years depreciation should be revised. Practice Question 29 When there is a change in estimated depreciation previous depreciation should be corrected.

Current and future years depreciation should be revised. As a result of change in any of these estimates entity will have to incorporate the change by in prospective manner ie. When there is a change in estimated depreciation.

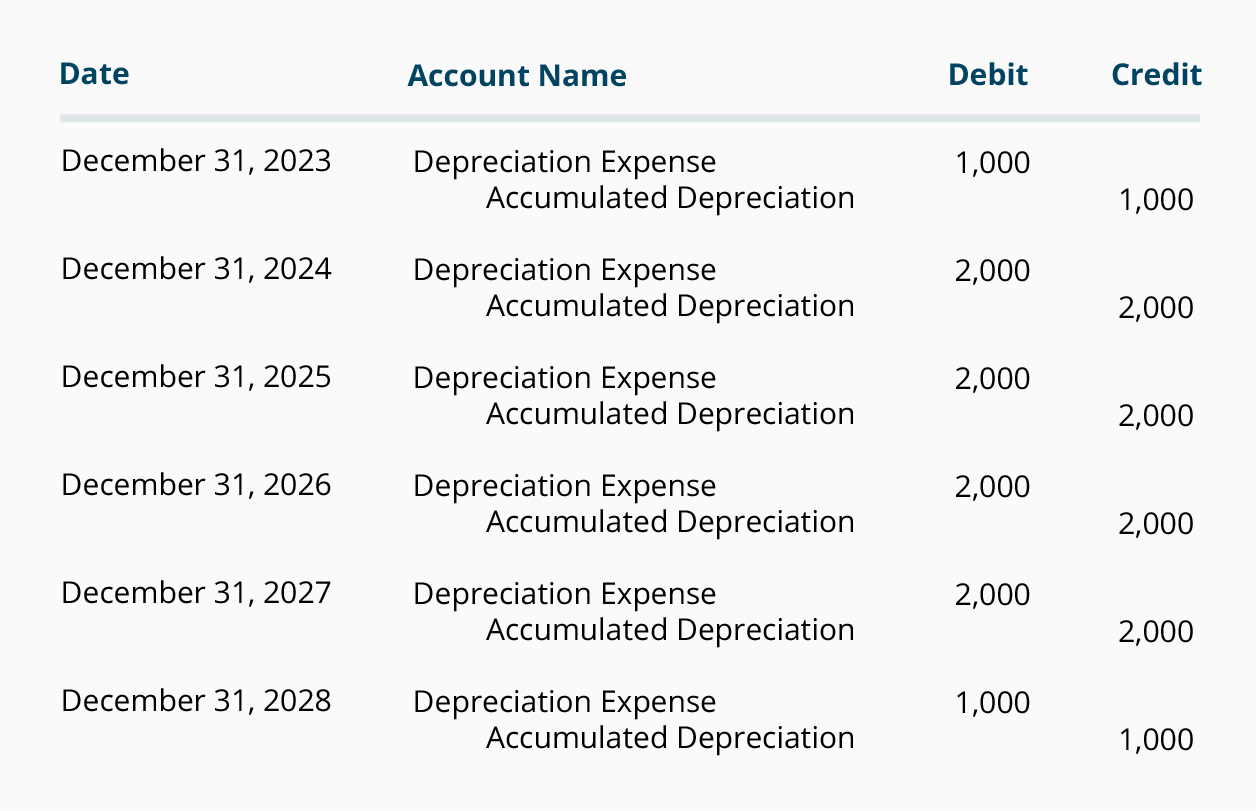

If there is a change in the depreciation estimate then the new depreciation expense must be computed and accounted for going forward. The effects of the change must be incorporated in the accounting period in which the estimates are revised.

Assets And Depreciation In Accrual Accounting G Vijaya

Activity Based Asset Depreciation Activities Asset Financial Management

Depreciation Formula Calculate Depreciation Expense

The Sum Of The Years Digits Method Of Depreciation Accounting Education Learn Accounting Method

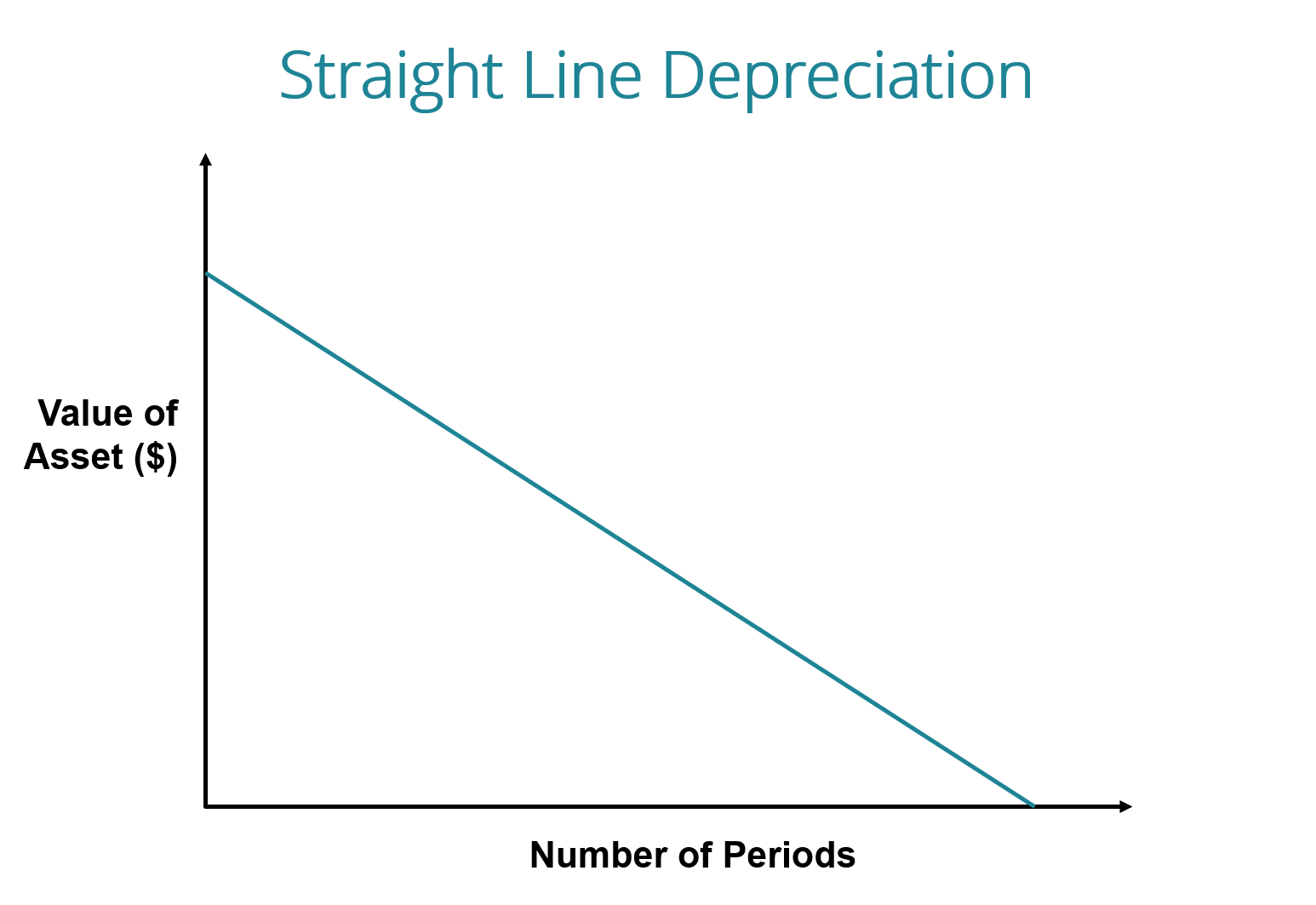

Straight Line Depreciation Accountingcoach

Straight Line Depreciation Accountingcoach

34k Jf1yo78n4m

Straight Line Depreciation Accountingcoach

Straight Line Depreciation Accountingcoach

The Small Business Accounting Checklist Infographic In 2021 Small Business Accounting Bookkeeping Business Accounting

Depreciation Methods Dummies

Changes In Depreciation Estimate Double Entry Bookkeeping

Learn The Revalution Method Of Depreciation At Http Www Svtuition Org 2013 07 Revaluation Method Of Depreciati Accounting Education Learn Accounting Learning

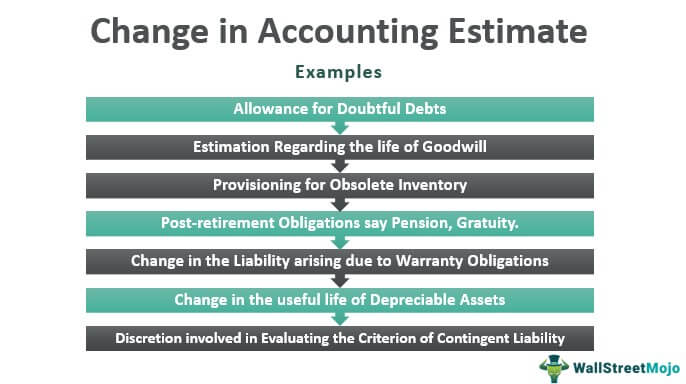

Change In Accounting Estimate Examples Internal Controls Disclosure

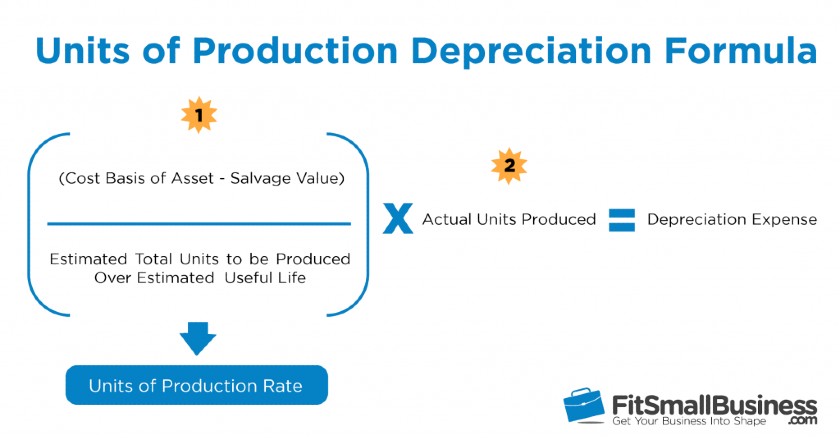

Units Of Production Depreciation How To Calculate Formula

Straight Line Depreciation Formula Guide To Calculate Depreciation

Small Business Accounting Checklist Pinterest

Unit Of Production Depreciation Budgeting Money Managing Your Money The Unit

Fixed Assets Depreciation Read Full Article Read Full Info Http Www Accounts4tutorials Com 2015 10 Fix Accounting And Finance Asset Management Fixed Asset

Posting Komentar untuk "When There Is A Change In Estimated Depreciation"